When it comes to saving for retirement, high income families have unique needs. The standard course of action is to maximizing contributions up to IRS defined limits into tax-favored accounts such as 401(k)s and IRAs.

However, additional contributions are needed for top earners to build a nest egg large enough to maintain their standard of living in retirement.

After maximizing retirement accounts, most then turn to taxable investment accounts. The main benefit of taxable accounts is that they are completely liquid, and they can also be used for any purpose. Accounts are funded with after-tax dollars and any interest, dividends, and capital gains incurred are taxed annually (the dreaded 1099.) These taxes can be managed with careful planning, including the use of tax efficient investments and asset location strategies.

But even with careful planning, there’s an inevitable tax drain on returns over the saver’s lifetime.

Is there anything else high-income families can do as a savings alternative?

Today, we’ll discuss Health Savings Accounts, a special tax-efficient vehicle that can improve retirement outcomes, as well as counter the rising cost of health care.

Health Care Costs Have Skyrocketed

The cost of health care in the US has steadily increased over the last 50 years. On a per capita basis, health spending has increased from $355 per person in 1970 to $11,172 per person in 20181.

Annual health insurance premiums have followed suit. In 2018, the average annual premium for a family covered under an employer-based plan was $19,616, while single coverage was $6,8962.

Health care costs are a significant detriment to savings because they both limit funds available for retirement accumulation and act as a drag on retirement cash flow.

Increasingly, employers, employees, and retirees are looking for ways to save on health costs and insurance premiums.

The solution may be high deductible health plans.

These plans generally offer reduced premiums since the burden of current year health care costs is transferred to the insured (up to a maximum dollar amount.) If you don’t require care in a given year, there are no out-of-pocket costs above your premium. But if you do incur significant expenses, you are responsible for your deductible and any portion of co-insurance expenses up to the policy’s yearly maximum.

Heath Savings Accounts

Health Savings Accounts (HSAs) were established in 2003 to give participants in high deductible plans a way to save for these deductibles and out-of-pocket expenses on a very tax efficient basis.

HSAs are considered the holy grail of tax-preferenced investment accounts because they deliver a powerful and unique triple tax benefit.

- Contributions to an HSA are tax deductible

- Earnings grow tax deferred

- Distributions can be taken tax-free for qualified medical expenses.

HSA funds can be used in any given year for deductibles, co-insurance, prescriptions, dental, and vision expenses.

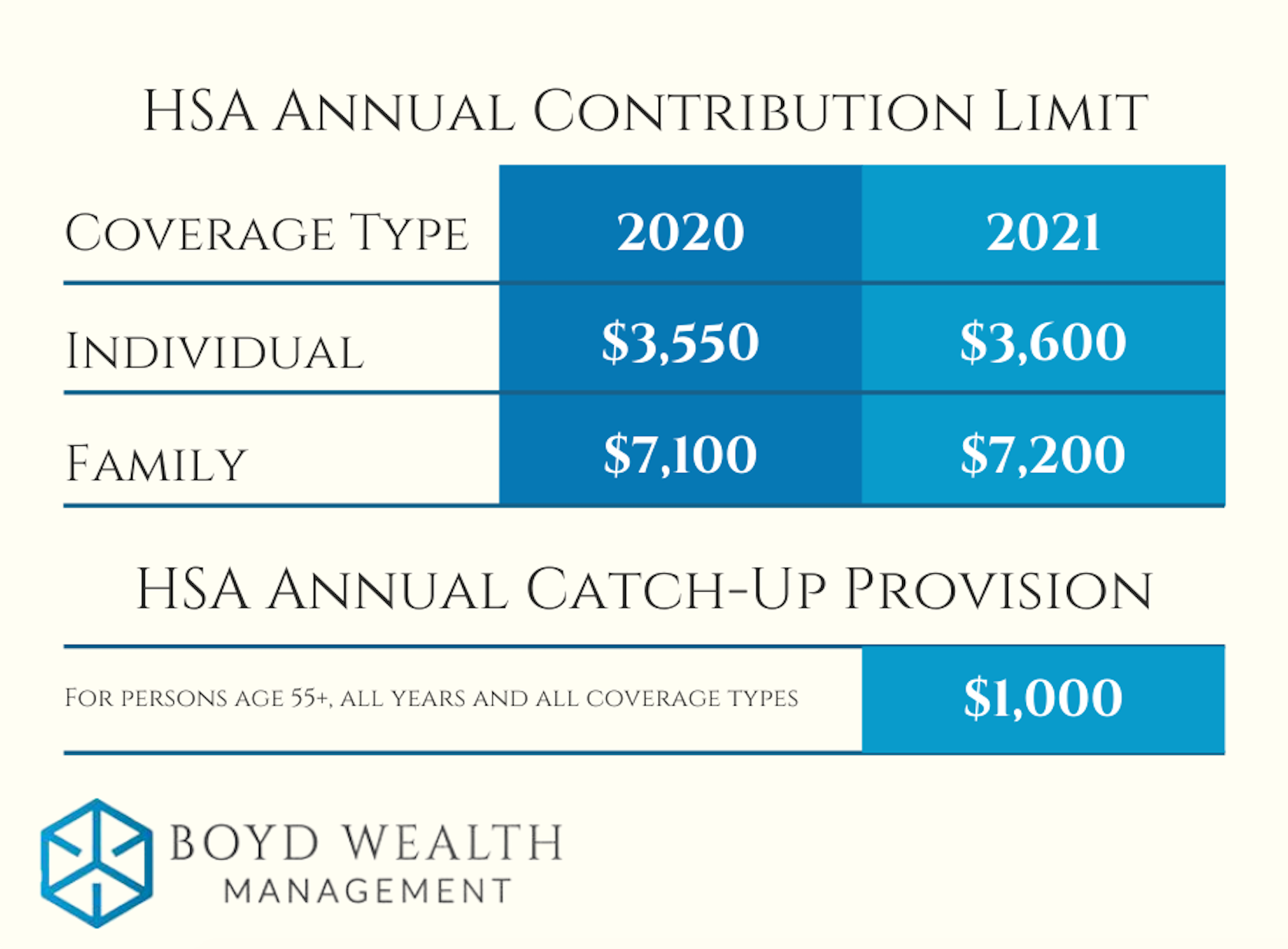

To be eligible to contribute to an HSA, you must be enrolled in a qualifying high deductible health plan. For 2020, this is defined as a plan that requires minimum annual out-of-pocket deductibles of $1,400 for an individual and $2,800 for a family. Yearly out-of-pocket expenses (including deductibles, copayments, and coinsurance) cannot be more than $6,900 for an individual or $13,800 for a family. You also must not be enrolled in Medicare, covered by another health plan that’s not a high deductible plan, or claimed as a dependent on someone else’s tax return.

The contribution limits for 2020 and 2021 are shown below and there are no income phaseouts:

Maximize Retirement Dollars

For a high-income earner, a family contribution of $7,100 may not seem like much, but the power of an HSA comes in the way you use it (or how you don’t use it.) Imagine contributing an additional $7,100 each year into an investment allocation of your choosing that compounds tax-free, and there’s no obligation on a year to year basis to use it.

For example, a 35-year-old couple could maximize contributions to this account every year until age 65. But instead of using their HSA to pay health care expenses along the way, they could opt to pay all their yearly expenses out-of-pocket.

Assuming a hypothetical average annual return of 8%, this $7,100 yearly contribution could accumulate an HSA balance of $804,310 by retirement age 65.

That would be a sizeable war chest at retirement to help cover health costs. Moreover, this dedicated account reduces the pressure on retirement assets intended to cover lifestyle funding during the golden years.

An HSA is not a use-it-or-lose-it strategy. You would save receipts for all those out-of-pocket costs incurred pre-retirement, affording you tax-free reimbursement anytime.

If you accumulate more in the HSA than you think you’ll spend during your lifetime, no problem: just reimburse yourself in retirement for that medical procedure you had ten years ago, as an example. With this method, you can take your contributions and compounded earnings out of the account tax-free, using it to fix the roof, go on that special vacation, or to supplement income.

HSA Providers

Like most plans, HSA providers vary in what they offer, their costs, and investment options.

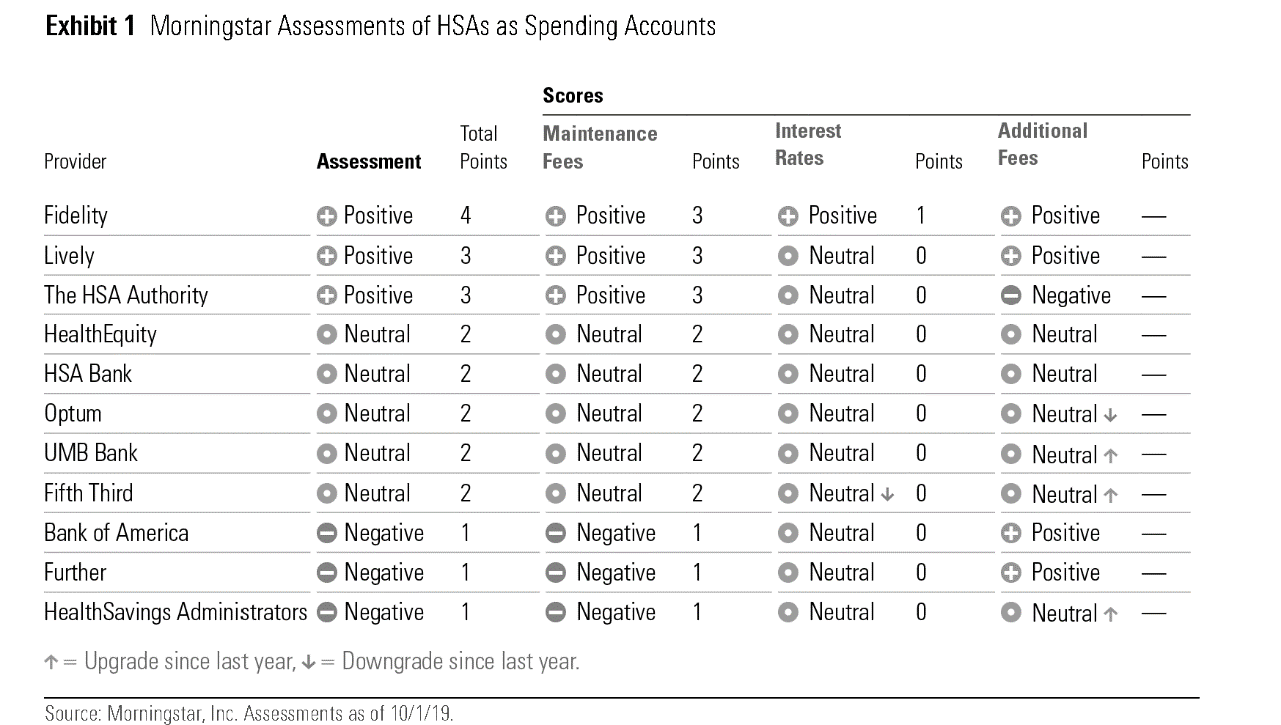

In an October 2019 study, investment research firm Morningstar analyzed and ranked 10 HSA providers.

“When evaluating the best HSAs for investing, we considered five components: investment menu design, quality of investments, price, investment threshold, and performance.”3

Here’s what they concluded:

Fidelity emerged as the clear winner. In interest of full transparency, my own HSA is at Fidelity, and I was impressed with the ease of set-up and investment offering.

From a planning standpoint, I like to leave enough in the cash account to cover one year of maximum out-of-pocket costs. I then invest the remainder in a growth portfolio for the future. I still pay all of my health care deductibles, co-insurance, prescriptions, dental, and vision expenses out-of-pocket, but the cash component provides peace of mind should I need to dip into the HSA.

Conclusion

High income earners have special needs when it comes to accumulating adequate resources to support their lifestyle in retirement. A properly used HSA can add one more dimension to creating financial security.

Due to the eligibility requirements, this strategy may not work for everyone. Further, those close to retirement age may not have a long enough runway to see the benefits of compounding.

However, for those that can take advantage of this tool, the advantage of having a dedicated health care bucket in retirement - and possibly an additional bucket of tax-favored cash to support spending goals - is clear.

Happy Planning,

Brian

Sources/Further Reading:

3. https://www.morningstar.com/insights/2019/10/23/best-hsa-investing