You’ve been paying into the system your whole life, with a portion of each hard-earned paycheck reduced for Social Security withholding. Of course, you haven’t had a choice, but it still hurts enough in the moment that you’ve long anticipated the payoff.

You have at least an idea of how Social Security retirement benefit work, but you’ve also heard that the whole system could soon be bankrupt.

What should you do?

I hope to answer some of your questions in this guide to the retirement portion of the Social Security system - how it works, when to consider claiming, and whether it will even be there for you.

According to a recent NY Times article, “the Social Security Old-Age and Survivors Trust Fund will now be depleted in 2033, a year earlier than previously projected.” The blame, like many things these days, lies with the pandemic. In addition to the vast amount of Baby Boomers already retiring, many older workers left the workforce early and accelerated their retirement due to the pandemic.

While technically the Social Security system will be insolvent in 2033, it is estimated that 76% of benefits will be able to be paid out unless Congress changes the rules. Modifications to shore up the system could include an increase in the Social Security tax rate workers and employers pay or moving full retirement age beyond the current age 67.

However, it’s hard to imagine any bill which cuts benefits to current retirees gaining traction in Congress. In fact, some 62% of beneficiaries 65 and older rely on Social Security for at least 50% of their retirement income. It may be political suicide to run for office on a platform that reduces these valuable retirement dollars to those that have paid into the system their entire working lives.

Source: Vanguard

So, if we assume that Social Security will mostly exist in its current form, then the question is, how do you best maximize your return for all those taxes you paid into the system?

How the Social Security Retirement Benefit Works

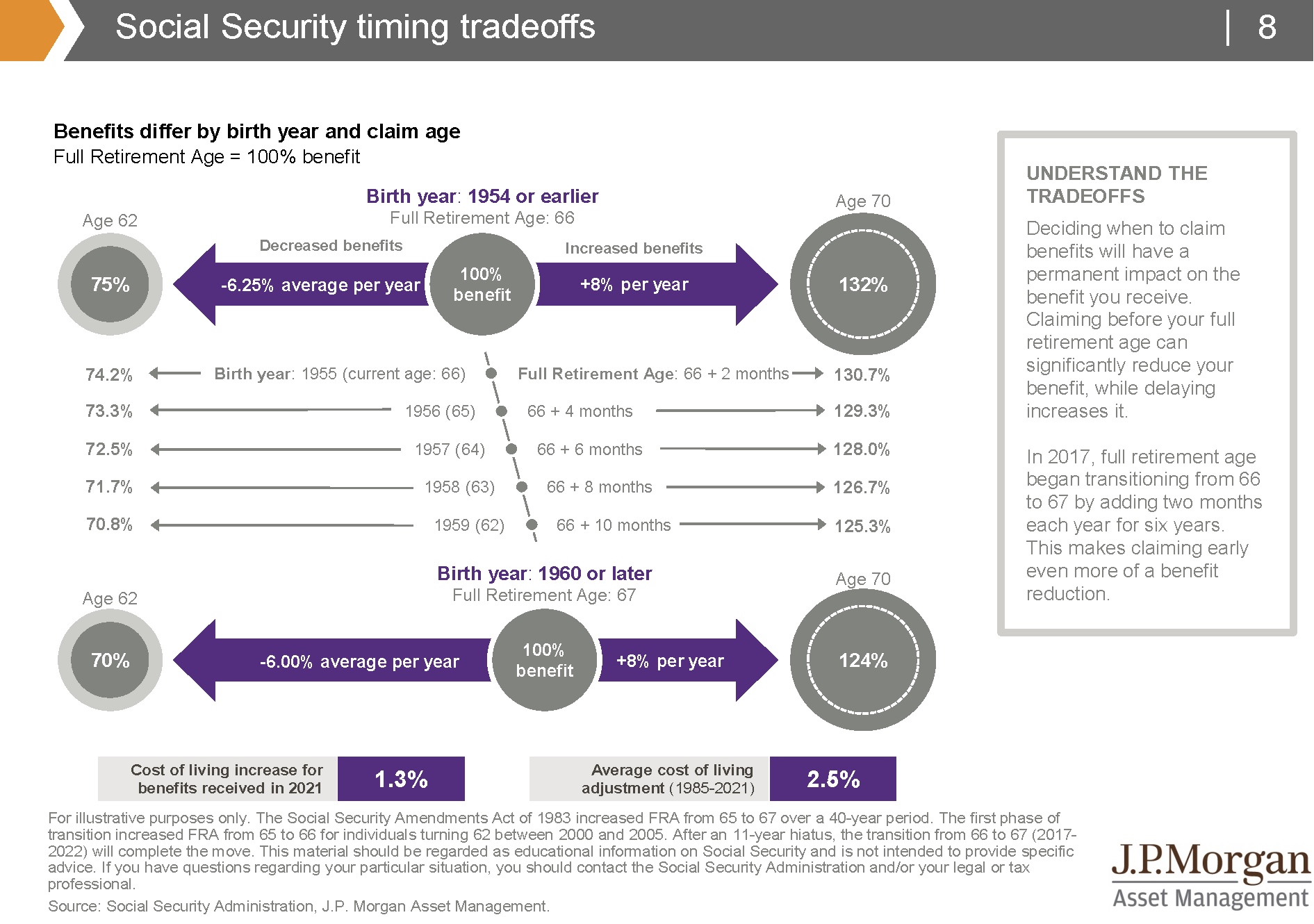

The earliest date you can begin collecting Social Security retirement benefits is age 62, but this comes with a reduction of between 70% and 75% of your full retirement benefit. The actual reduction depends on your year of birth, as you can see in the excellent chart below from JP Morgan Asset Management.

Full retirement benefits are available between age 66 and 67 (based on year of birth.) This is known as your full retirement age (FRA).

You have the option to delay Social Security retirement benefits to age 70 in exchange for an enhanced benefit of between 124% and 132% of your full retirement number. To put it simply, delaying benefits results in an 8% increase in payout for every year past FRA up to a cap at age 70. There is no benefit to delaying past age 70.

Factors to Consider When Timing Your Social Security Benefits

There are several things to consider with any discussion about when to take Social Security retirement benefits. Those include:

1. Need

If you have retired from active work and had limited or no other sources of retirement income, you may consider taking Social Security early.

2. Longevity

You might consider taking early benefits if you and your spouse have poor life expectancy.

Someone claiming at age 62 (without a strong financial need to do so) must be expecting to only live to age 77 for that to work in their favor financially. Otherwise, the reduction in benefit from claiming early will penalize them the remainder of their life.

Someone claiming at a full retirement age of 66 years and 10 months (in this example) would be better off waiting to collect until at age 70 to maximize benefits if they expect to live beyond age 80.

For a married couple, the odds that at least one of them is still living at age 77 is 94%. The odds of at least one of them being alive at age 81 is 86%. For most people, those odds are compelling enough to delay benefits as long as possible.

3. Employment

If you’re still employed and collect benefits prior to full retirement age (FRA), your benefits will be temporarily reduced.

- If you begin collecting between age 62 and FRA and you earn more than $17,640, your benefit will be reduced by $1 for every $2 earned.

- Once you reach FRA, any benefits withheld will be returned in the form of higher monthly payments.

- In the calendar year in which you reach FRA your benefits will be reduced $1 for every $3 if your earned income exceeds $46,920. Again, any benefit withheld will be returned in the form of higher monthly payments.

- At FRA or later, there is no reduction in benefits regardless of how much you earn. In fact, if you haven’t qualified for maximum benefits, then working after FRA can result in higher benefits when you do claim. Additionally, working longer gives you more time to accumulate tax-deferred assets in retirement accounts.

The bottom line is that if you’re still working, it pays to delay benefits as long as possible.

4. Taxes

Retirees with moderate to high incomes will likely pay federal income taxes on a portion of their benefits. Up to 85% of Social Security benefits would be eligible for federal income taxation according to a formula based on Provisional Income (PI).

Thirteen states also impose a state income tax on Social Security benefits. These states are Colorado, Connecticut, Kansas, Minnesota, Missouri, Montana, Nebraska, New Mexico, North Dakota, Rhode Island, Utah, Vermont, and West Virginia. Surprisingly, California is not one of them!

As you can see in the chart above, claiming benefits while still employed and earning a reasonable income can result in an erosion of benefits due to taxation.

5. Expected Rate of Return

There is a case to be made for claiming early and receiving a lower benefit because you expect to invest your check and earn a high rate of return.

For example, someone reaches early retirement at age 62 and anticipates living only to age 80. They expect to earn a healthy 10% annual rate of return by investing their benefit.

Using the chart above, doing so is more advantageous than waiting to collect either their FRA benefit or waiting to age 70.

But as previously discussed with longevity, the longer you’re expected to live, the more the math points to delaying benefits to age 70, even with a solid return.

On an important side note, the real consideration is how difficult it may be to earn 8%, 9%, or 10% in an all-stock portfolio. And while the S&P 500 has averaged 10.50% per year since 1990, that came with a healthy dose of volatility.

*US recessions are noted in grey.

We expect returns to be muted going forward for a number of reasons, including high current equity valuations and persistently low interest rates.

Below, we find the current expected future returns for a US all-stock portfolio from 2 major investment managers:

Moreover, bonds have been in a bull market since interest rates peaked in the 1980s. A balanced portfolio of 60% stocks and 40% bonds has averaged 8% since 1995.

It’s best to expect a diversified portfolio of stocks and bonds to deliver just 3%-6% going forward.

For most people with solid retirement resources and reasonable longevity, waiting to take Social Security until age 70 years will likely yield the highest payout.

6. Emotion

The optimal financial plan doesn’t exist in a vacuum. Emotions don’t show up on a spreadsheet. The ‘best’ strategy is unique to each individual, based on their own set of needs and circumstances.

Social Security timing is one of those decisions where you may accept trade-offs. We’ve talked about the math, but there is also deep emotion involved in the decision on when to claim.

We’ve heard from many that they may deeply regret the decision to delay benefits. They recall a lifetime of paychecks with 6.2% of their income withheld for the Social Security Trust Fund. For those that are self-employed, the withholding has been twice that. They are ready to collect.

For someone set on taking benefits before FRA or age 70, we fully recognize and acknowledge those feelings. But we will also test your financial plan under different claiming scenarios so you can decide how best to move forward.

Bottom Line

Even though the Social Security Trust Fund is now projected to be “insolvent” by 2033, I do believe the system will exist largely in its current form. Therefore, your attention is best focused on how to maximize your accumulated benefits as one piece of your long-term financial security in retirement.

While there is no one-size-fits-all approach, the data points to delaying benefits as long as possible for most high-net-worth families.

So, what can you do right now to positively impact your Social Security picture?

- If you’re pre-retirement and it’s been a while since you’ve reviewed your Social Security benefits, you can create an online account here. (If you read our cyber protection piece and placed a freeze on your credit, you’ll want to do a temporary unfreeze to get through the sign-up process on the ssa.gov site.)

- If you’re pre-retirement, please reach out so we can discuss the facts, the math, and your feelings. Then, we can model how the different claiming options may affect your retirement plan.

- And if you’re currently in retirement and already collecting benefits, enjoy that monthly check -you’ve no doubt earned it!

Please reach out if we can be of any assistance planning for your Social Security retirement benefits or if we can help in the process of claiming your benefits with the Social Security Administration.

Happy Planning,

Brian